GitLab IPO: Which Version Control Systems Will Benefit?

Continuing Our Analysis of the GitLab IPO Filing

Resuming our examination of the GitLab IPO documentation, initiated last Friday, we will dedicate further attention to its details.

This week is anticipated to be active in terms of initial public offerings, with Toast and Freshworks scheduled to finalize pricing on Tuesday following the market closure and commence trading on Wednesday. Expect comprehensive analyses of each company’s valuation and performance upon their market debut.

IPO Landscape and Upcoming Events

The Exchange team will endeavor to secure interviews with the respective CEOs. However, due to the concurrent Disrupt conference, operations will be somewhat more demanding.

The Exchange focuses on startups, financial markets, and investment capital.

Access it daily on Extra Crunch or subscribe to The Exchange newsletter delivered every Saturday.

Shifting our focus to the present, we are revisiting developer platform GitLab and its forthcoming IPO. We will begin by identifying the venture capital firms poised to benefit from the public offering.

For added perspective, we will also revisit the acquisition of GitHub by Microsoft, utilizing historical data shared by GitHub’s former CTO to estimate the deal’s current value if it were to occur today.

Extrapolation and Financial Review

This will necessitate some degree of projection. Finally, we will analyze GitLab’s recent quarterly performance data to determine if a focused review of its operational results yields valuable insights.

Our aim is to provide a thorough and engaging analysis!

GitLab's Extensive Investor Portfolio

As a privately held entity, GitLab successfully secured substantial funding – exceeding $400 million, according to Crunchbase data. This capital was raised in progressively larger amounts, beginning with the company’s initial seed funding rounds in 2015 and continuing through its Series E round in late 2019.

Khosla Ventures initially spearheaded the company’s early investment phases. Subsequently, GV, Goldman Sachs, and ICONIQ Capital assumed leading roles in later funding rounds.

Consequently, these firms are prominently featured on GitLab’s major shareholder list. The following details, derived from GitLab’s S-1 filing, outline share counts and ownership percentages for investors holding more than 5% of the company’s stock:

- August Capital: Possesses 14,931,200 Class B shares, representing 11.1% of that particular equity class.

- GV: Holds 8,888,776 Class B shares, equivalent to 6.6% of the same equity class.

- ICONIQ: Owns 15,472,204 Class B shares, constituting 11.6% of that equity class.

- ICONIQ: Also controls 1,150,784 Class A shares, representing 100% of that equity class (subject to dilution during the IPO).

- Khosla: Maintains 19,028,320 Class B shares, or 14.1% of that equity class.

Considering GitLab’s valuation of $6 billion in a recent secondary transaction, these percentages translate into significant financial stakes. August Capital, for instance, is projected to realize gains exceeding $600 million at that valuation.

This potential return surpasses the total capital of the firm’s $450 million Fund VII.

The upcoming GitLab IPO is poised to generate substantial returns for numerous investment funds.

A key aspect of this situation involves estimating GitLab’s potential valuation upon its public debut. The company’s rapid Annual Recurring Revenue (ARR) growth – at 69% – positions it among highly valued public software companies. GitLab could achieve a valuation exceeding $6 billion, further amplifying the returns for the aforementioned firms.

This outcome exemplifies the potentially lucrative nature of venture capital investing. Other, smaller investors in the company are also anticipated to benefit significantly. At a $6 billion valuation, Khosla could potentially gain over $1 billion.

A $10 billion valuation would substantially increase these returns.

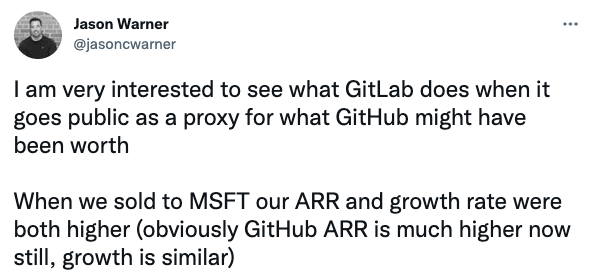

These figures highlight how comparatively inexpensive the Microsoft-GitHub acquisition now appears, as noted by GitHub’s former CTO:

Considering its larger revenue base and faster growth rate, GitHub would likely be valued higher than GitLab if assessed today. The difference would be substantial.

Microsoft acquired GitHub for $7.5 billion, suggesting they secured a remarkably favorable deal given current software valuation standards.

Generally, previous software exit prices now appear low in light of the increased valuation of software revenue since the beginning of 2020. The market now recognizes a higher intrinsic value for software, resulting in many earlier transactions occurring at what could be considered discounted rates today.

While acknowledging that large-scale transactions are always positive, the shift in SaaS valuations does introduce complexities when making comparisons.

GitLab's Performance Review

The eventual pricing structure for GitLab will be significantly influenced by its past performance data. Our previous analysis centered on the company’s H1 2021 results, covering a two-quarter timeframe. This analysis will now shift focus to a more detailed examination.

Below is a breakdown of GitLab’s revenue performance on a quarterly basis:

The data presents both positive and negative aspects. Let's begin by addressing the concerns.

The data presents both positive and negative aspects. Let's begin by addressing the concerns.Reporting a net loss that nearly triples revenue in a recent quarter is not ideal, particularly as the company prepares for its public debut. While GitLab’s income statement showed improvement in the quarter ending April 30, 2021, the final quarter of its fiscal year was considerably weaker. Furthermore, the increase in GitLab’s losses during the quarter ending July 31, 2021, compared to the previous quarter, does not inspire confidence.

We previously observed that the company’s operating losses for the first half of 2021 were less substantial than those of the first half of 2020, considering calendar periods loosely aligned with fiscal periods to avoid repetitive use of the term “fiscal.” However, a similar optimistic outlook is difficult to maintain when examining the company’s net losses.

On a more encouraging note, GitLab achieved a new record in revenue growth during its most recent quarter. The following details the gains to its top line for each quarter, starting with the period ending July 31, 2020:

- $4.8 million (July 31, 2020 quarter).

- $7.8 million (October 31, 2020 quarter).

- $4.0 million (January 31, 2021 quarter).

- $3.8 million (April 30, 2021 quarter).

- $8.2 million (July 31, 2021 quarter).

The latest GitLab quarter demonstrated significantly higher sequential revenue growth than the corresponding period in the previous year. Investors seeking a growth narrative within GitLab – and willing to delve deeper than its recent aggregated half-year results – may find evidence of it here.

Another positive trend can be identified. Observing GitLab’s growth in customers spending six figures annually reveals the following:

- January 31, 2020: 173.

- January 31, 2021: 283.

- July 31, 2021: 383.

This represents an increase of 100 customers over a year, followed by another increase of 100 customers in just half a year, which is a strong indicator. This growth is partially attributable to the company’s robust net-dollar retention, as highlighted in our initial review of the company’s IPO filing. Essentially, GitLab’s success in upselling its services to existing customers naturally leads to an increase in larger accounts.

However, the acceleration in the rate at which customers reach or surpass that spending threshold – or transition into that category – doubling in pace so rapidly is a decidedly bullish signal.

Looking forward, the release of an initial price range is anticipated. Once available, we will conduct more rigorous calculations and provide a more detailed analysis. Further updates will be provided shortly!